Macro Commentary

Markets continued to recover in the second quarter (“Q2”) as governments around the world continued to add stimulus and liquidity to economies. The S&P/TSX Composite Index gained 16% in Q2 while the S&P 500 gained 20% (or 15.8% in Canadian dollar terms given the decline in the U.S. dollar). The Technology sector led the market's performance with many technology companies seeing accelerated demand from work-from-home and data/bandwidth consumption trends. Many technology companies also have a higher percentage of recurring revenue via subscription-based business models, which help protect earnings in times of uncertainty. Consumer stocks also performed well as consumer spending shifted towards the home and away from restaurants and travel. Gold was also a strong performer while Financials under-performed as low interest rates negatively impact bank earnings.

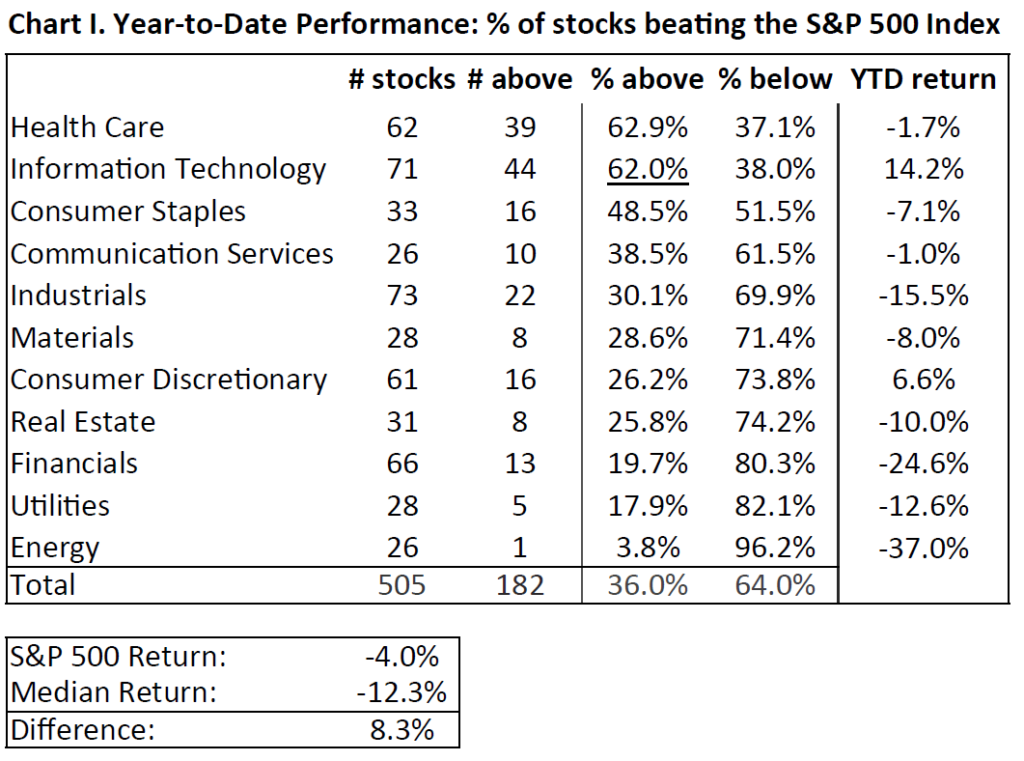

Turning to first half results, a closer look at the S&P 500 shows a meaningful negative skew to the market's performance. Specifically, nearly two thirds of the stocks in the S&P 500 have under-performed the Index's return (Chart I). Simply put, most stocks are not keeping up with the overall market's returns. The skew is so notable that there is a 8.3 percentage point difference between the S&P 500 return (-4.0%) and the mean (midpoint) return of -12.3%.

Portfolio Commentary

Taking it down to the portfolio level, our core investment principles have not changed: protect and grow our investors' capital through discounted valuations, strong balance sheets, high quality management teams and attractive business environments. Top performers* in Q2 were IPG Photonics (“IPGP” +45.5%), Quest Diagnostics (“DGX” +41.9%) and Middleby (“MIDD” +38.8%). IPGP, a leader in fiber laser technology, moved higher as manufacturing in China has started to gain momentum. The company has a strong technology leadership position and has a long runway of growth opportunity as fiber lasers replace more traditional manufacturing processes. Quest Diagnostics is a leading provider of diagnostic testing and has delivered approximately 20% of all US-based COVID-19 testing. We also see a strong growth pipeline with Quest as it consolidates the industry through acquisitions and organic growth given its lower cost structure. Lastly, Middleby's stock recovered after a sharp decline in Q1 given its food-service exposure.

As we outlined in our March note, we are looking at the market's dislocation for opportunities to further improve the quality of businesses we own in the Fund. One such stock was added to the portfolio in Q2: Visa (“V”)*. Visa is a leading global electronic payments network that helps move money between financial institutions, merchants and individuals in more than 200 countries. In 2019, Visa processed more than 138 billion transactions worth $11.4 trillion on its more than 3.4 billion cards globally. Visa has grown free cash flow and dividends at 13% and 20% compound annual growth rates, respectively, over the past five years. We expect management to continue creating significant shareholder value based on a long runway of growth opportunities combined with Visa's strong competitive position within the global payments industry. Growth drivers include: i) increasing penetration of contactless cards in the U.S.; ii) Visa's leading business-to-business payments network, which represents an incremental $70-$100 billion revenue opportunity and at higher margins than consumer payments; iii) Visa Direct, Visa's real-time payments system that powers seven of the major peer-to-peer payments platforms in the U.S. such as PayPal, Square and Zelle. Visa has consistently held a high market share of global payments despite strong competition and a wave of new entrants. The cost of building and running a global payments network leaves new payment players with few options other than to partner with incumbent players. Lastly, it's important to note that Visa does not take any credit risk (i.e. it's the banks that take the risk of consumers not paying). Visa simply makes money on the number and dollar value of transactions flowing over its network.

Looking Forward

While U.S. Gross Domestic Product fell 32.9% in Q2, the steepest decline since the government started keeping records in 1947, the tug-of-war between government stimulus and economic contraction has thus far been one-sided with government stimulus driving market Indices towards all-time highs.

Companies have started to report second quarter earnings, key themes are as follows: Q2 is likely the low point for earnings for most companies; many companies are targeting permanent cost savings from real estate and travel; the pandemic has accelerated many in place trends, especially around technology; companies selling products related to the home have seen strong demand at the expense of travel-related expenses; companies are focused on employee safety, financial liquidity, and meeting customer needs through this uncertainty; companies with decentralized decision making have navigated the uncertainty well as employees that are closer to the customer have the ability to make decisions to adjust the business; companies remain cautious with guidance, especially with COVID-19 flare-ups occurring in the U.S. and the prospects of stimulus checks ending; investors seem willing to look beyond short-term pain for companies that have strong competitive positions and growth prospects.

We will continue to look for opportunities resulting from COVID-19 related disruption.