Here are the Key Takeaways:

- Bank of Canada Cautious on Rate Cuts: The recent rate cut to 3.75% aligns with inflation targets, but further aggressive cuts are unlikely given the forecast for stable growth and rising wages.

- Resilient U.S. Economy: Strong personal consumption and unexpected gains in retail sales and GDP indicate continued economic momentum, contradicting predictions of a cooling labour market.

- Rising Wage Pressures: Significant wage settlements in the U.S. point to persistent wage-driven inflation, challenging the outlook for falling inflation rates.

- Shift in Inflation Trends: Core goods deflation has reversed, contributing to inflationary pressures, while Supercore inflation (core services excluding shelter) remains elevated.

- Bear Steepening in U.S. Yields: The Fed’s accommodative stance is driving higher long-term yields, leading to a “bear steepening” of the yield curve as the focus shifts from inflation containment to growth.

Bank of Canada Rate Cut

On October 23, 2024, the Bank of Canada reduced its policy interest rate by 50 basis points (bps), from 4.25% to 3.75%, aligning with market expectations based on recent inflation data of 1.6% year-over-year. However, the Bank projects inflation to average near 2% and growth above 2% by 2025-2026, setting a high bar for additional aggressive cuts. The recent employment report showing a 4.9% year-over-year increase in average hourly wages further reduces the likelihood of extensive rate reductions.

U.S. Economic Indicators

The U.S. economy continues to exceed market expectations. September retail sales, particularly in the “Control Group” (which excludes food, energy, gas, and building materials), rose by 0.7%, far above the 0.3% forecast. Strong personal consumption fueled Q3 GDP growth to an annualized 2.8%, with businesses likely to replenish depleted inventories, supporting growth into Q4.

Despite forecasts of labour market softening, the September unemployment rate fell to 4.1%, and wage growth remained robust, with average hourly earnings up 0.4% month-over-month and 4.0% year-over-year. Wage settlements, such as the longshoremen’s 62% increase over five years, signal potential for continued wage-driven inflation. As the saying goes, “prices follow money,” indicating that inflation is more likely to rise than fall.

Inflation and Core Goods

Post-COVID demand surges in goods led to rising inflation, followed by a moderation as demand normalized. Recent data show that deflation in core goods has ended, contributing to September’s higher-than-expected CPI. Additionally, the Supercore inflation measure (core services excluding shelter) remains elevated and continues to climb, highlighting persistent price pressures in key sectors.

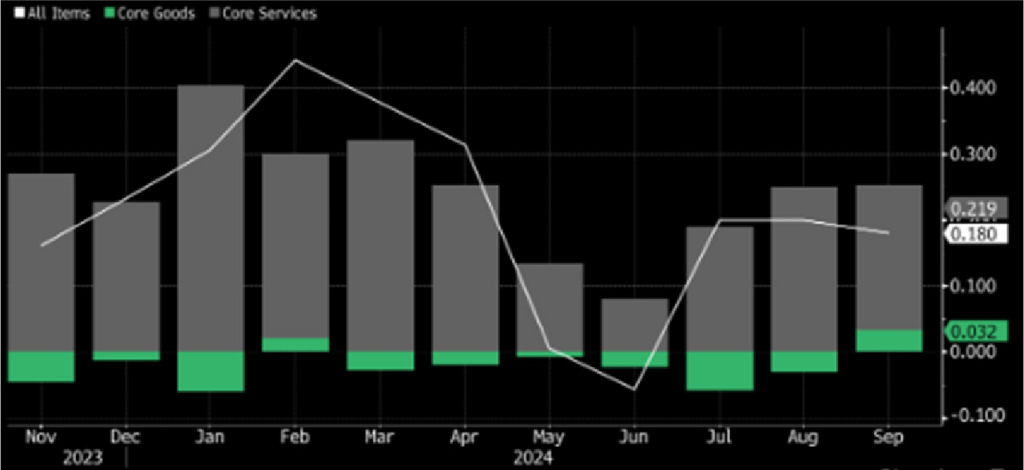

Goods Inflation Comes Back

After months of negative prints

Source: Bloomberg, September 2024.

Supercore Measure Continues to Climb

Price Pressure in core services less housing are rising

Source: Bloomberg,

September 2024.

U.S. Dollar and Canadian Dollar Vulnerability

Following the Fed’s 50 bps cut on September 18, markets initially priced in another 200 bps of cuts through 2025. However, robust economic data have scaled back these expectations, with the November 7 cut of 25 bps bringing the anticipated further cuts down to just 75 bps into 2025.

Fed’s Easing Path and Market Expectations

The Fed’s ongoing rate cuts and the shift toward growth have bolstered risk assets and long-term U.S. yields, strengthening the U.S. dollar, especially against the Euro and Canadian dollar. A breach of key support for the Canadian dollar at 71.50 U.S. cents could lead to a decline toward previous lows around 68.00 U.S. cents.

Perspective on Yield Curve: “Bear Steepening”

Yield curve normalization appears underway, with the Fed likely to continue easing. The “super easy” policy stance will drive stronger growth and higher inflation, pushing up longer U.S. yields and resulting in a “bear steepening” of the yield curve. Since September 17, the U.S. 10-year Treasury yield has risen by 77 bps, from 3.60% to 4.37%, with further increases anticipated.

Source: Thomson Reuters, October 2024.

The commentaries contained herein are provided as a general source of information based on information available as of September 30, 2024 and should not be considered as investment advice or an offer or solicitations to buy and/or sell securities. Every effort has been made to ensure accuracy in these commentaries at the time of publication however, accuracy cannot be guaranteed. Market conditions may change and Caldwell Investment Management Ltd. accepts no responsibility for individual investment decisions arising from the use or reliance on the information contained herein. Investors are expected to obtain professional investment advice.

Published on November 21, 2024