June Recap:

The Caldwell Canadian Value Momentum Fund (“CVM”) performed in-line with the S&P/TSX Composite Total Return Index (“Index”)1 over the second quarter, having declined 13.0% versus a decline of 13.2% for the Index. Over the month of June, CVM declined 10.4% versus a decline of 8.7% for the Index. Industrials (-1.1%) and Utilities (-2.9%) were relative outperformers over the past month, while Health Care (-18.0%), Materials (-14.8%) and the Energy (-11.9%) sector lagged. Aside from the Health Care sector, which was dragged down by the continued sell-off in cannabis names, weakness in the Materials and Energy was generally brought on by recession concerns and the resulting negative impact to commodity prices.

From an attribution standpoint, June was a challenging month in which every sector within the Index declined. Aside from cash holdings, fund performance was aided by Capital Power (“CPX”, +0.2%), which continued to benefit from strong end market demand given supply/demand dynamics for power pricing in Alberta and Ontario. Additionally, the company remains committed to growing its renewable generation platform and its portfolio mix continues to shift away from coal-fired power generation well ahead of federal targets (zero coal power generation by 2030). We believe supply demand dynamics will remain favourable for the foreseeable future in light of the retirement of aging power plants across Canada and significant contracts coming up for renewal over the next few years. With industry leading efficiency at one of its major natural gas plants and a growing mix of renewable generation capacity, CPX is in a good position to win more than its fair share of upcoming contract renewals.

For the second quarter of 2022, Cenovus (“CVE”, +18.0%), Tourmaline (“TOU”, +19.2%) and cash holdings were leading contributors to fund performance2. CVE and TOU both benefited from higher energy prices (for most of the quarter) and solid earnings reports. Leading performance detractors were Karora Resources (“KRR”, -47.8%), Airboss (“BOS”, -56.1%) and Tricon (“TCN”, -33.9%). KRR sold off along with lower gold prices. Lack of visibility regarding new award timing and ongoing supply chain issues make BOS’ medium term growth outlook challenging, which in turn led to significantly reduced earnings estimates. Lastly, despite strong demand for single family rentals in the U.S., higher interest/mortgage rates could pressure TCN’s ability to earn an appropriate return on its portfolio of single family rentals. Given the company’s growth ambitions, future property purchases may not share the same economics as homes purchased over the past two years at near rock bottom rates.

During the month of June, the Fund initiated positions in Dollarama (“DOL”) and Boralex (“BLX”). DOL is one of Canada’s leading discount retailers. The company continues to execute in a challenging environment as highlighted by its most recent earnings report. Despite inflationary headwinds and tight inventory levels, the company posted a strong top and bottom line beat. Same store sales growth metrics for the current year are tracking towards target while longer term, DOL is continuing to execute on its organic growth strategy of expanding its store base by approximately 6% annually. Lastly, with its attractive price points and a strong focus on value, DOL is benefiting from the current trade-down trend. BLX is an independent renewable energy power producer operating nearly 2,500 megawatts of production capacity in North America, France and the UK. The company’s North American pipeline looks promising with active request for proposal bids that would significantly expand capacity in New York and Quebec. In France, elevated spot power prices could drive significantly higher cash flows and returns in the near term while upcoming contract renewals with the French government would support higher cash flows over the medium term.

The Fund held a 34% cash weighting at month-end. CVM has generated substantial value to investors over its long-term history driven by the combination of strong company-specific catalysts and a concentrated portfolio. We continue to look forward to strong results as we progress through 2022 and beyond.

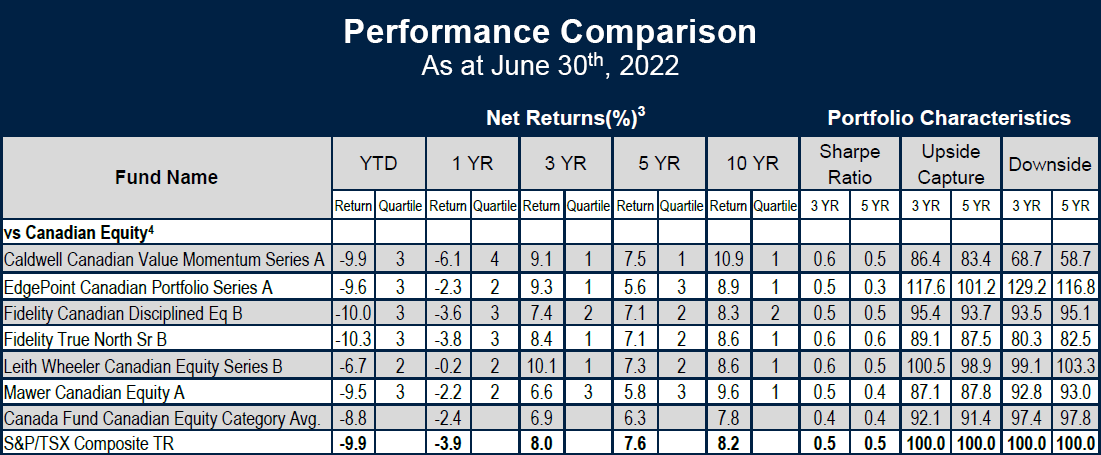

CVM Performance Comparison as at June 30th, 2022

2Actual Investments, first purchased: CVE 1/6/2022 , TOU 6/11/2021.

3Return since August 15, 2011 (Perf. Start Date): CVM (Series A) 9.7%, Index 6.9%. | Returns are annualized for periods greater than one year.

4Categories defined by Canadian Investment Funds Standards Committee (“CIFSC”).

The CVM was not a reporting issuer offering its securities privately from August 8, 2011 until July 20, 2017, at which time it became a reporting issuer and subject to additional regulatory requirements and expenses associated therewith.

Unless otherwise specified, market and issuer data sourced from Capital IQ & Morningstar Direct. As the constituents in the CIFSC Canadian Equity category largely focus on securities of a larger capitalization and CVM considers, and is invested, in all categories, including smaller and micro-cap securities, we have also shown how CVM ranks against constituents focused in the smaller cap category. The above list represents 6 of a total of 395 constituents in the CIFSC Canadian Equity category.

The information contained herein provides general information about the Fund at a point in time. Investors are strongly encouraged to consult with a financial advisor and review the Simplified Prospectus and Fund Facts documents carefully prior to making investment decisions about the Fund. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Rates of returns, unless otherwise indicated, are the historical annual compounded returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not guaranteed; their values change frequently and past performance may not be repeated.

FundGrade A+® is used with permission from Fundata Canada Inc., all rights reserved. The annual FundGrade A+® Awards are presented by Fundata Canada Inc. to recognize the “best of the best” among Canadian investment funds. The FundGrade A+® calculation is supplemental to the monthly FundGrade ratings and is calculated at the end of each calendar year. The FundGrade rating system evaluates funds based on their risk-adjusted performance, measured by Sharpe Ratio, Sortino Ratio, and Information Ratio. The score for each ratio is calculated individually, covering all time periods from 2 to 10 years. The scores are then weighted equally in calculating a monthly FundGrade. The top 10% of funds earn an A Grade; the next 20% of funds earn a B Grade; the next 40% of funds earn a C Grade; the next 20% of funds receive a D Grade; and the lowest 10% of funds receive an E Grade. To be eligible, a fund must have received a FundGrade rating every month in the previous year. The FundGrade A+® uses a GPA-style calculation, where each monthly FundGrade from “A” to “E” receives a score from 4 to 0, respectively. A fund’s average score for the year determines its GPA. Any fund with a GPA of 3.5 or greater is awarded a FundGrade A+® Award. For more information, see www.FundGradeAwards.com. Although Fundata makes every effort to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by Fundata.

Publication date: July 13, 2022.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.

- Caldwell Investment Management Ltd.