Bond Strategy Update August 2016

“Defender of the Realm (i.e. Your Portfolio)”

Overview

Experimental monetary policies have driven interest rates to zero (and then some) and unleashed countless “unintended consequences” that we have yet to deal with.

One phenomenon that we are all living with is the destruction of interest income. With this comes the relentless search for yield, often at the expense of risk and sound judgment. Asset bubbles are everywhere and, while the going is (still) good, we need to start looking for protection.

“Bond Bubble?”

One bubble that is often cited is the “bond bubble”. It is one of the most misleading phrases being thrown around, and we need to ‘set the record straight’.

To be sure, the issuance of corporate debt (often called corporate bonds) has skyrocketed since central banks started ultra accommodative monetary policies. From the several years leading up to the Great Financial Crisis (2003 – 2008) to now, corporate bonds outstanding have doubled. As a result of more stringent capital and liquidity ratios imposed by Basel III, Dodd Franks and the Volcker Rule, U.S. large dealers’ corporate bond holding capacity has shrunk by 75%. The ratio between outstanding corporate bonds and holding capacity dropped from 1:1 before 2008 to 8:1 now. Making it worse, surveys by the Federal Reserve on Primary Dealers revealed that actual holdings by Primary Dealers, who are the market makers for these corporate bonds, routinely fell below 10% of their capacity. The ratio is actually 80:1.

It is quite obvious the corporate bond market, with the Primary Dealers as market makers, will not be able to absorb any meaningful selling, should selling begin.

The good news is, the selling has not started. The bad news is, it will come someday soon, and the market structure is broken. Therefore, as far as corporate bonds are concerned, there is a ‘bubble’.

We at Caldwell are not fond of corporate bonds. We strongly believe a fixed income portfolio should be able to mitigate risk from the overall stock market, thereby isolating the Alpha (or extra returns) that our equities managers can produce. Corporate bonds carry corporate risk, which is synonymous with equities risk and are therefore unable to perform this task.

To be able to achieve this, the fixed income portfolio needs to have government bonds of the highest credit quality. We like the AAA-rated Federal Government of Canada bonds and Treasury Bills.

Bloomberg recently reported, that according to estimates by prominent asset allocators and actuaries, there is a pent-up demand of roughly US$3 trillion for U.S. government bonds, or Treasuries. We looked up the “Flow of Funds Report”, published by the Federal Reserve every quarter, and found that “Defined Benefits Pension Funds” only hold 6.3% of Treasuries in their asset mix. That is an extremely low percentage for conservative entities like pension funds with fixed, long-term liabilities. We are trying to find out the situation in Canada, which should not be dramatically different. From the last quarterly earnings reporting, Canadian life insurance companies are being told by their actuaries that they are underinvested in government bonds.

Therefore, there is no ‘bubble’ in government bonds. Demand will be strong going forward.

Bonds, or Treasury Bills?

During our conversations with clients and institutional investors, we are often asked, “Why bonds? Their yields are so low!”

To be sure, we are fixed income managers, not bond defenders. There are times when we like bonds (when we expect bond yields to fall, bond prices to rise) and there are times when we hate bonds (when we expect bond yields to rise, bond prices to fall) and we hold Treasury Bills instead. This is the essence of our active management approach.

Ultimately, we are in love with the AAA credit rating of Federal Government of Canada bonds, which carries no credit risk and offers great security in a highly uncertain world.

Macroeconomic Roundup

The U.S. economy continues to sputter along. Occasional surges in consumer spending have not been matched with capital investment spending. As long as this pattern persists, employment and wage growth will not maintain momentum, and slow, uneven growth will be the result. Case in point, U.S. GDP averaged 1.2% on an annualized basis for the past four quarters. Without wage growth, the outlook for inflation remains subdued. The overall environment is bond friendly, but timing, as always, is important.

Canadian data have been ‘better-than-feared’ even with an expected 11.0% decline in capital investment in non-energy manufacturing sectors for 2016 (from a survey by Statcan). The danger here is that much weaker data await us for the balance of the year.

The Bank of Japan, even with extremely aggressive monetary policies, failed to get inflation up. Different measures of inflation hover around the zero mark; deflation fears loom large.

The European Central Bank’s (“ECB”) latest quantitative easing program is underway, this time buying corporate bonds. After driving government bond yields in core EU countries to near or below zero, the ECB is running out of bonds to buy.

China continues to guide the Yuan lower versus the U.S. dollar. The lower Yuan helps China to export its excess commodities-related intermediate goods to the rest of the world in its latest effort in “destocking”. This will put a lid on commodities prices.

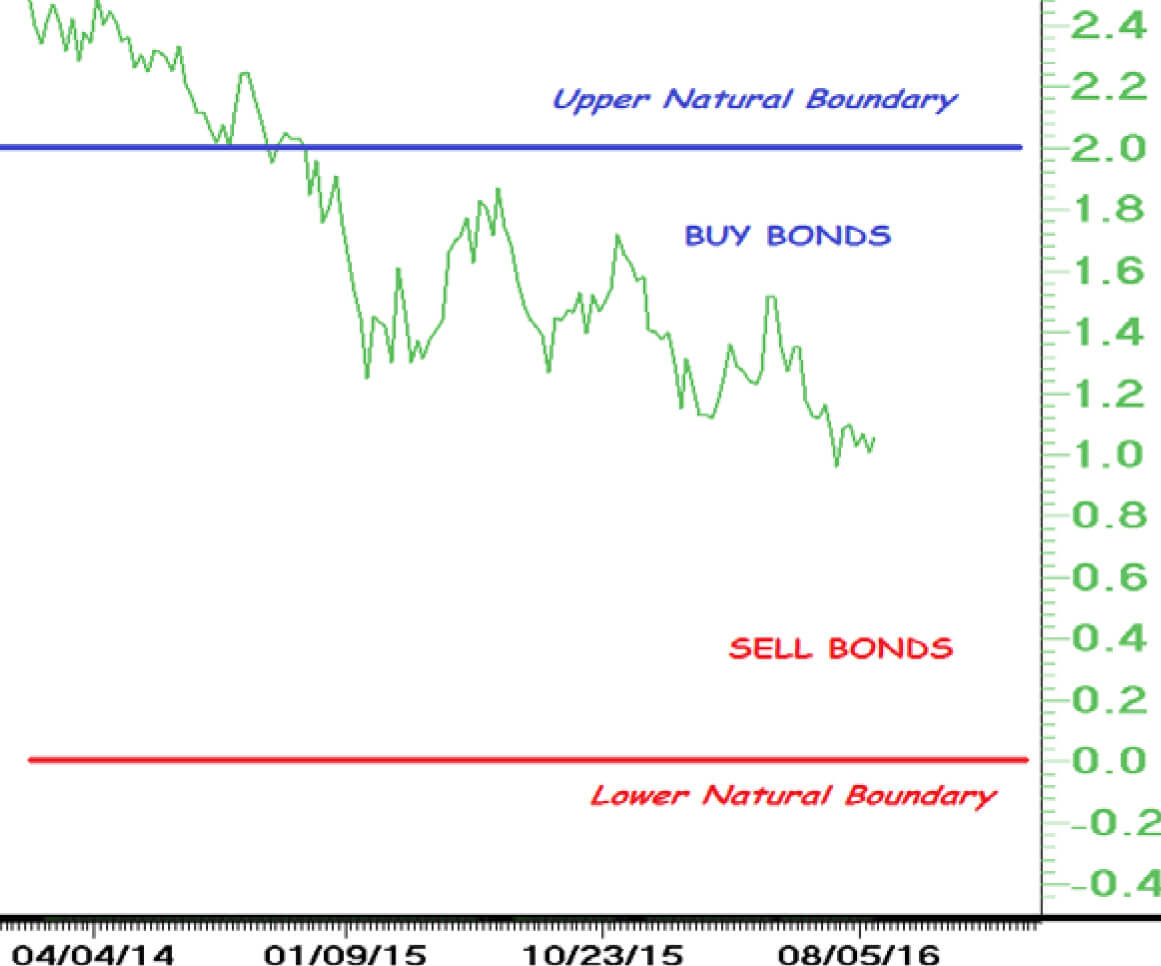

Our “Natural Boundaries of Interest Rates”

Our “Natural Boundaries of Interest Rates” are shifting lower as softer economic data come in. The “Natural Boundaries” of the Government of Canada’s 10-year bond yield should be 0.00% to 2.00%.

Bond Strategy

The macroeconomic backdrop is very supportive for Government of Canada bonds. Demand is also rising among foreign investors, who are wrestling with government bond yields that are lower than those of Canada.

We will be looking for buy signals from technical analysis to accumulate Government of Canada bonds within the context of the “Natural Boundaries of Interest Rates” (chart below) in anticipation of bond yields to fall/bond prices to rise, we are looking for capital gains when bond yields fall towards the lower boundary by dominant macroeconomic forces.

Caldwell-Bond-Strategy-Update-Aug-2016