Management Update TMX: UDA.UN January 2017

Equity markets in North America pushed higher in January while international markets gave back some of the large December gains. The U.S. (S&P 500) closed up 1.8%, Canada (S&P/TSX Composite Index) trailed its neighbor to the south, up 0.6%. Europe (Euro Stoxx 50) lost -1.8%, and Japan (Nikkei 225) lost -0.4%.

The markets have been given a lot to digest since President Trump entered office. The hardest to swallow might be having a politician who so closely follows through with what he promised in his campaign. President Trump did not mince words that certain “sacred cows” of the last quarter century, specifically globalization and free trade, would be examined and possibly repealed. President Trump’s voter base, especially in rust belt states, saw a rapid emigration of their manufacturing jobs to places like Canada, Mexico, China and the Pacific Rim. These folks did not participate in the large wealth creation period that occurred over the last twenty five years due to their low exposure to financial assets and declining median real income. In fact, one could even make the argument that large current account deficits to China helped spur the housing collapse and financial crisis, as cheap credit poured into the U.S. through enormous capital account surpluses. The focus will now be to enact pro-growth policies for this political base as they are the key to maintaining the majority in the House of Representatives (“House”) and the Senate in 2018. These policies seem to be rooted in protectionism, de-regulation, and tax reform.

In his first day in office, President Trump withdrew formally from the Trans Pacific Partnership (“TPP”) and signaled his intention to renegotiate the North American Free Trade Agreement (“NAFTA”) at the appropriate time. This most likely has more implications for Mexico as the White House has stated that Canada is at a very low risk of suffering collateral damage from any NAFTA discussions. In fact, on this same very first day, President Trump signed executive action to move forward on both the Keystone XL and Dakota Access pipelines. The Keystone XL pipeline will extend all the way from Hardisty, Alberta to Houston, Texas. This is excellent news for the Province of Alberta which predominantly produces heavy sour crude. This heavier crude oil requires specific refiners who are capable of processing it and are abundant in East Texas, near the Gulf of Mexico. The refineries of East Texas are built to refine the heavy sour crude that comes from Latin America, specifically Venezuela. Given the fragile political environment of Venezuela, Western Canada Select (“WCS”) heavy oil could see increased demand and a rise in price.

Speaker of the House, Paul Ryan, has been pushing for a sweeping overhaul of the U.S. tax system. The current corporate tax system in the U.S. is ineffective as most corporations use tax havens to shelter profits along with loopholes and deductions to lower their effective tax rate. Due to this antiquated system, domestic businesses are overtaxed and uncompetitive with their developed-market peers. This has shifted jobs and investment abroad with the middle class taking the brunt of this. Speaker Ryan’s plan has four key features:

- Lowering Corporate Tax from 35% to 20%

- Allow for full deprecation of new capital expenditures in its first years rather than over many

- Disallowing businesses from deducting interest expense

- Assess taxes through a territorial tax system

Now that both House and Senate are controlled by the Republican Party, this is their chance to pass Ryan’s tax plan into law. The idea is to pay for tax cuts by transforming the current corporate income tax system into a Destination-Based Cash-Flow Tax (“DBCFT”) by using a Border Adjustment Tax (“BAT”) to incentivize businesses to invest and manufacture in the U.S. The current tax system in the U.S. is on global corporate income tax (Global Revenue – Global Costs). The new system is destination based where the government taxes corporations on domestic corporate income tax (Domestic Revenue-Domestic Costs). This means revenues and costs earned abroad are ignored by the Internal Revenue Service (“IRS”). The BAT comes into play by effectively being a tax on imports and subsidy to exports, while differing from a VAT, by also allowing companies to write off wages as costs and furthering the incentive to increase the labour force. Under the current BAT outline, exporting companies will receive rebates in excess of the tax they would have paid on foreign profits (had the product be manufactured abroad). The outlined BAT system incentivizes domestic manufacturers to build excess capacity and over export to optimize revenue and export tax credits. This could have sweeping effects on U.S. industrial production and investment while creating a long overdue rise in real median income for the middle class.

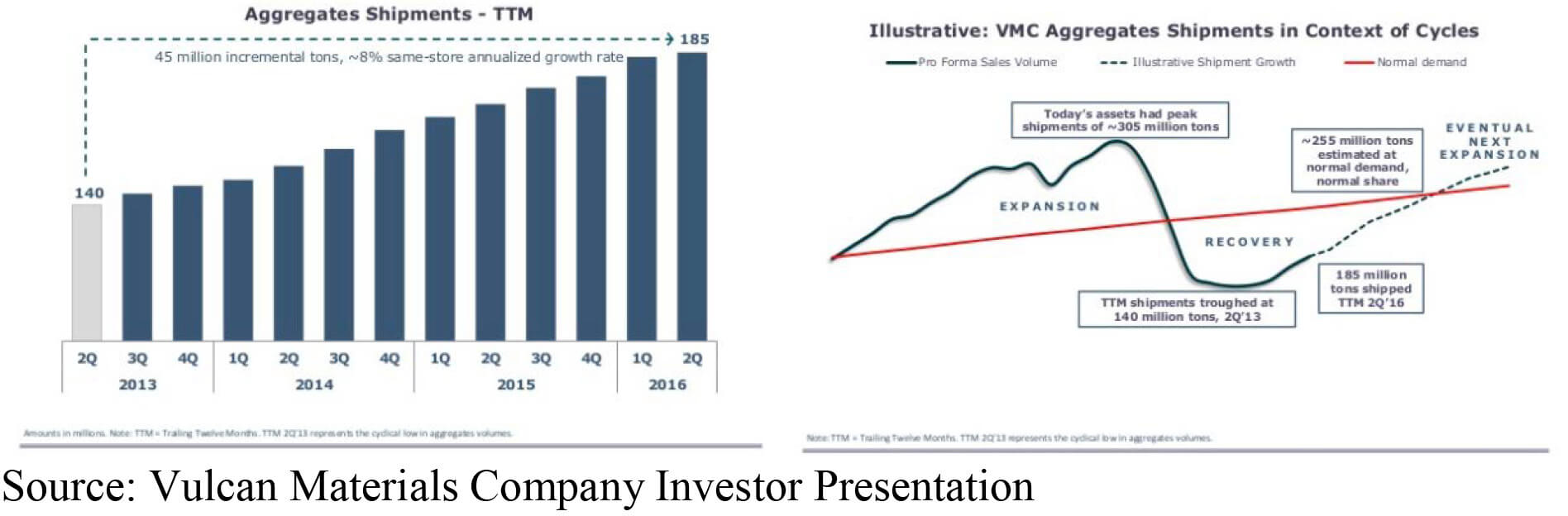

Increasing the domestic output of the U.S. will require building out America’s industrial capacity. This cannot be accomplished without improving the infrastructure that underpins it. President Trump’s proposal for infrastructure investments of $1 trillion adds to the five-year $305 billion transportation infrastructure bill that President Obama signed into law in December 2015. The main criticism of President Obama’s 2015 Infrastructure Act was that it would not even keep up with the deterioration of U.S. infrastructure. Vulcan Materials Company (NYSE:VMC) is the nation’s largest producer of construction aggregates (primarily ready crushed stone, sand, and gravel) and a major producer of asphalt mix and ready mixed concrete. Aggregates are used in virtually all types of construction projects including highways, water and sewer systems, industrial manufacturing facilities and other non-residential buildings, railroad ballast as well as non-construction industrial and agricultural applications. Over the last three years, VMC has seen its aggregates shipments increase 8% per year to 185 million tonnes from 140 million tonnes. This is far below the 255 million needed just to get to normalized demand that keeps up with population growth and depleted existing infrastructure. In 2016, VMC saw the value of new projects entering its pipeline grow 88% to $253 billion from $134 billion.

In 2012, VMC initiated a Profit Enhancement Plan (“PEP”) to divest non-core assets, improve earnings and cash flows, pay off debt and thereby, strengthening its overall credit profile. Currently, VMC is operating around 50-60% capacity in its business lines. They possess huge operational leverage as their current backlog is converted into revenues. With 75% of the U.S. population growth from 2010 to 2020 projected to occur in VMC served states, a disproportionate amount of new federal government projects should find its way into their pipeline. The projects that VMC sees coming are multiyear in nature and backed federal transportation legislation that provides relatively stable funding.

We believe that VMC will be a strong performer in 2017. Increased highway construction awards and an extension of state Department of Transportation should act as a catalyst to drive earnings for the rest of the decade. Fundamentals support that the energy sector will grow faster than the overall economy as global energy supply and demand comes back into balance.

Unitholders are reminded that the Caldwell U.S. Dividend Advantage Fund offers a Distribution Reinvestment Plan (“DRIP”) which provides Unitholders with the ability to automatically reinvest distributions and realize the benefits of compounded growth. Unitholders can enroll in the DRIP program by contacting their Investment Advisor.

CUSDAF_January-2017ManagerCommentary